12.27.2016

Why Dollar Strength Is Actually A Good Factor For US Economy?

Christopher Wood, strategist for CLSA Asia-Pacific Markets, has turned bullish on China amid cautious optimism as Donald Trump enters the White House. Woods has also said that If the Trump story really follows through, it’s a better story for small-cap stocks in America. If the dollar remains strong, it will be a negative for Asia and emerging markets. But in my view, this dollar strength won’t persist in all of 2017. It may peak when Donald Trump walks into the White House., according to a story in newsmax.

(http://www.newsmax.com/Finance/StreetTalk/christopher-wood-trump-china-asia/2016/12/26/id/765630/?

Another story in CNBC says that President-elect Donald Trump's shock comment that the dollar is too strong suggests the U.S. is about to declare as dead a two-decade policy of publicly favoring a strong currency. There's no question that the Trump administration would not want a strong dollar. A strong dollar does nothing good for whatever Trump is basically trying to do," said David Woo, Bank of America Merrill Lynch's head of global rates and foreign exchange research. "Yes, the U.S. fundamental story is bullish for the U.S. dollar, but the problem here is they actually don't want a strong dollar. I think it's going to go up. However, it's going to be a much more volatile climb."

(http://www.cnbc.com/2017/01/17/trump-just-signaled-death-of-clinton-era-strong-dollar-policy.html)

However, the anecdotal evidence suggests otherwise. In a paper titled Dollar power: The economic and market implications of a strong dollar, Dan Morris notes that Fears of a strong dollar are unwarranted. The rising value of the US currency reflects the relative strength of the US economy. (https://www.tiaa.org/public/pdf/PM_and_TL_Dollar+WP+2015-02-25_RBS.pdf)

The paper says that the recent swift rise in the dollar; more than 10 % since May 2014 and twice that since 2011 has raised worries about the impact on the U.S. economy and financial markets. The concern is that a strong currency will reduce U.S. exports and lead to slower economic growth. This fear is misplaced for several reasons. First, it confuses cause and effect. The value of the dollar reflects the strength of the U.S. economy relative to its trading partners. As long as the U.S. continues to grow at a faster pace than much of the rest of the developed world , the dolla r is likely to continue gaining in value. It is true that U.S. net exports would be lower than if the dollar had not appreciated, but the U.S. economy is not very trade dependent. Goods and services e xports account for only 13% of GDP , compared to nearly 50% for Germany. In fact, because the U.S. is a net importer, its economy benefits more from cheaper imports than it loses from more expensive exports . Companies gain as the cost of imported materials and machinery falls, while consumer s see lower food and product prices in stores.

12.21.2016

Demonetization: Ruchir Sharma Does Not See Any Economic Argument Behind Decision

In one of the best critiques of the Demonetization decision, renowned economist Ruchir Sharma stated that he doesn't see the economic argument for this decision. He expressed that these kinds of measures are taken when a country is going through some major crisis, a financial crisis, some inflation crisis. India too this step outside of a crisis environment and he thinks that most people in private will tell you whether it is government or business people that they don’t really see any enduring economy benefit of this. A very lengthy interview by the master throws open a number of possible outcomes for global financial markets in coming year. He does not pull punches and opined that as far as India is concerned we have pulled back in terms of the fact that it is a very difficult time to be in many countries because there are very few countries where the prospect looks any good. He hits the nail on the head when he states that in the boom period of 2003 to 2007 - there were about 50-60 economies in the world which were registering growth rate of 7 percent or more every year. This year that number is down to 5-6 percent, so economic growth is lower everywhere and in particular across emerging world.

India needs to match the corp tax rate with US: Ruchir Sharma

http://www.moneycontrol.com/news/fii-view/india-needs-to-matchcorp-tax-rateus-ruchir-sharma_8145081.html#discontent_div

If one were to look out for 2017, the momentum currently is with the developed markets and China still remains the biggest risk to the global economy is the word coming in from author and investor Ruchir Sharm, Chief Global Strategist and Head of the Emerging Markets Equity, Morgan Stanley Investment Management.

"It takes a debt of USD 4 to create USD 1 GDP growth in China," says Sharma in an exclusive interview to CNBC-TV18's Shereen Bhan.

Most surveys indicate a sharp pullback for US economy, says Sharma, adding that with economic momentum returning to developed economies it could be negative for emerging markets. Moreover, with US talking about reducing corporate tax rate to as much as 15-20 percent could be a big negative for emerging markets because investors then would naturally flock to US market.

So if emerging market like India wants to attract capital then reducing corporate tax rate is very crucial. "India needs to match the corporate tax rate with the US," he adds. India will also have to reduce its dependence on external funding for growth.

Moreover, the growth models of most emerging markets are seriously under threat especially with the way global economy shifting and deglobalistaion process already on, believes Sharma.

With regards to demonetistaion in India, he says outside observers are surprised at the move because normally this kind of a step is undertaken when a country is in severe crisis like a financial one or inflation.

He says, if the move was to end corruption then one could have undertaken more organic steps to curb that because there is no developing economy in the world where corruption is not a major issue.

According to him, it is tough to understand the current situation in India and the impact of demonetistiaon on the gross domestic product (GDP) at the current stage. He says, most business people that he has met in India are talking about a 30 percent impact due to demonetistaion and are downgrading earnings for FY17.

So, it would be tough to see high earnings growth in FY18 too with so many economic disruptions, says Sharma. An avid follower of elections in India, he says for Uttar Pradesh elections caste would be the main factor and not so much demonetisation.

Below is the verbatim transcript of Ruchir Sharma’s interview to Shereen Bhan on CNBC-TV18.

Q: In terms of India the biggest factor to deal with this at this point in time is demonetisation. You have been fairly critical, you believe that this kind of therapy was not justified; you also believe that if you look at the cash to gross domestic product (GDP) ratio then it is not outrageously high at 12 percent to GDP for India. In fact you believe it is comparable to other economies like China, Thailand etc, you have said that revenge cannot be a development strategy and India cannot leapfrog in that sense by using demonetisation as the route. Do you buy any of the economic arguments or the government is presenting that yes there will be short-term pain but in the long-term this structurally changes the India story?

A: No, I don’t see the economic argument for this. I think that the debate is now shifted now whether there is any political benefit to this. I think that a lot of people in India have been surprised at least outside observers by how well India has coped with this, that this is a huge step to be done in a non crisis environment. Usually, these kinds of measures are taken when a country is going through some major crisis, a financial crisis, some inflation crisis. However, this step has been taken outside of a crisis environment. I think that most people in private will tell you whether it is government or business people that they don’t really see any enduring economy benefit of this. The best case that I have heard about this that this was a lot of pain for nothing which is that you have got a lot of pain but the enduring benefit will not really be there from economic stand point.

Everyone now is debating when will this economy get back to some sort of normalcy because I have been meeting a lot of business people in the last couple of days I have been in India and the common number I have heard from everyone is down 30 percent. Roughly, if you look at all the sort of evidence in terms of sales or other things or if it is advertising, retail etc the most common number I have heard is that things are down about 30 percent from a year ago this month. So, December is really the pinch month for this. I think that most people agree that the benefits of this, people spoke about a fiscal windfall and other things, I think most people now come and conclude that none of that will be there. However, the debate now is shifted to politics which is that is there some political benefit to this.

Q: Do you believe that there will be political benefit?

A: I think it is early to say and I think that this is where we are really in unchartered territory because I had come to believe that in India over the last couple of decades the political paradigm had shifted that in this country now good economics was good politics. If you sort of deliver a high economic growth, low inflation you will get elected if you didn’t you would get booted out like the previous government got booted out. So, United Progressive Alliance (UPA) won one of the back of a very good economic track record for growth and inflation.

UPA to was a disaster in terms of growth and inflation, corruption like other factor, but really growth inflation just stick to the basics and it got. So, that was working at a state level as well that different states that we travel to that was working. I am not sure what is going on in India today which is that because this is such an emotive issue, it is like almost like saying you are going to end terrorism. Who can argue against that, we want to end black money, we want to end corruption like we want to.

However, my experience having travelled to different countries is the fact that it is very difficult to end these things in such a manner that these things are done more organically over time. There is not a single developing country I go to where corruption is not a major issue. Like two weeks ago I was in Mexico, and it was very interesting what was going on out there. In Mexico today the single biggest factor which anyone will speak to you about is corruption - corruption like in the political system. However, here is what happened in the year 2000 they introduced a state funding of elections. There is a big talk about that in India too that listen the next follow up step needs to state funding of elections.

Q: Or cleaning up at least political funding

A: However, in terms of, but this is one of the solutions to that which I have heard about but here is the problem with this. So, like in Mexico they introduced that in the year 2000 because they were closed to United States that what we should do have state funding and free television space to all the political parties. 16 years later today they think that corruption is way higher in the political system than it was in when they first introduced this. So, that to me is the point that these symptoms of a very high share of a parallel economy, very high use of cash in the economy or things like basic stuff like corruption these are the unfortunate plights I feel that many developing countries suffer from.

It is only as they get richer or more prosperous that you find that these traits sort of come off that you begin to move to a more normal environment. This is my case as far as India is concerned that we are at a very basic level of economic development. Our per capita income is just USD 200 at this level of development all we have to do is to follow the best practise of what the other countries have done to have got in less poor and more prosperous. We don’t have to reinvent the wheel out here that is something for economies that are technological frontier to try and do that to come up with new thing like in United States or other economics, they have to spend a lot on research and development to come up with new things because they have already reached a very high level of development.

At our level of development we don’t have to do this. We just have to basically stick to the basics and get those basic correct. I think that the real problem which I think that we face from is that we tend to be quite insular. Like last decade I felt that one of the biggest mistakes that policy makers made in India was to confuse the global boom with a local boom. That all emerging markets were booming and the rising tide lifted everybody and we thought that something special was going on here where really it was a global boom which was lifting us.

Similarly out here these type of experiments whether it is demonetisation or other thing are being carried out in other countries – political funding of elections all we have to do is to basically look at what other countries are doing and what the global trends are. The other thing which I found very fascinating is that this decade the amount of cash being used in the global economy has in fact gone up. So, now you think that the entire global economy is moving towards less cash or digitisation etc. However, this decade the amount of cash being used in the global economy has moved up significantly in many countries.

In countries like Japan in fact the cash or the share of the economy is 20 percent, so we are at 12; they are at other extreme of 20 percent. My point here is that why is this happening, so Japan is a classic case. When you have very low interest rates or the real interest rates are virtually nothing or negative and there is less faith in the banking system people tend to keep more cash and that has what is happen in Japan as well. We have seen a such a surge in cash take place. Now corruption I don’t find that much of a relationship with that Japan is hardly a corrupt society at 20 percent cash or the share of the economy.

Similarly Pakistan’s cash or the share of the economy is less than ours or less than 12. I don’t think Pakistan is a less corrupt state than what India is. So, I think that this is about sort of just learning and incorporating what other countries are doing and following those examples. So, if you are less insular and use other templates in terms of what is going on I think the results for us will be better. Now this has happened, there is no point sort of going about this, it is time to move on in terms of what are the next big issues that we need to deal with what is the next big start. Here I again find that what is happening in the United States today with the new President out there the implications of that are very significant including for India, some huge implications to that.

Q: The evidence at this point in time on the actual impact on the economy is largely anecdotal. You talked about 30 percent, it's what you are hearing and that is the common refrain when you talk to businesses in India, but what do you think will be the implications for the GDP in the short-term and do you believe that this is going to be more than two quarters, is this going to be a protracted slowdown that we should brace ourselves for. What is your sense because there is no precedent to talk about?

A: Absolutely and so therefore it is hard to predict because even GDP data is like a whacky data, for example someone told me that because the number of deposits in the system has increased furiously - that in fact will show an increase in GDP growth because the financial sector will show that the GDP growth has picked up significantly because the number of deposits has gone up significantly. So just looking at the GDP data - that's very quirky. So I do not think that we are going to see the effects of that.

My hope is that India is a very resilient economy that it is able to withstand lot of shocks. It goes back to my original point that a level of development is very basic, so we are able to withstand these shocks and we move on. The problem though is that that people haven't adjusted the expectations much, for example speaking to my team here about what the earnings expectations of the market is and I find that's staggeringly high; people have barely cut their earnings for this fiscal year, they are still expecting 10-11 percent type of growth. The first half was 3 or 4 or something and for next year they expect 18 percent growth in earnings.

Q: You believe that it's not realistic?

A: It just seems very high. We have got so much economic disruption going on, some of it is even justified expecting GST etc to come and it seems as if this move basically, for now at least, has killed a lot of animal spirits in the economy but a lot of entrepreneurs, traders are feeling that they have been labelled as just being crooks in terms of this and a lot of uncertainty about what will happen in the future. So this has killed a lot of animal spirit in the economy but to forecast what the exact path of this will be. Nobody knows. So therefore even in the market place we are seeing complete confusion, complete lack of activity, people have sort of step back.

Q: As an emerging market investor, what would the India call be today?

A: As far as India is concerned we have pulled back in terms of the fact that it is a very difficult time to be in many countries because there are very few countries where the prospect looks any good and there is one statistic which captures for me - in the boom period of 2003 to 2007 - there were about 50-60 economies in the world which were registering growth rate of 7 percent or more every year. This year that number is down to 5-6 percent, so economic growth is lower everywhere and in particular across emerging world.

Q: But relatively we are still doing better?

A: No but this is where I think we are missing the point - markets and investors respond to change, not to absolute levels. In the developed world economic momentum is coming back, like in USA the dramatic improvement in sentiment since Trump got elected on the market place is staggering, no one would have expected that.

Q: Record highs for the Dow.

A: Yes and apart from that you look at all the services, consumer confidence, business confidence, massive bump and the rally in the US stock market today, I think I saw this data and currently this is the best rally that the stock market enjoyed after the election of any President in American history. So this is really sort of huge surge in animal spirits going on in the United States. The other surprise is Europe; an economy that people written off, even their economic momentum is accelerating. Japan too is coming back from the brink. So in the developed world what we are seeing is economic momentum is coming back.

Q: So that is bad news than for emerging markets in terms of flows?

A: Yes in a way and that is what we are seeing currently which is that the dollar is supreme and the only giant sucking sound, we have heard so far, is of money going back to the United States and that is something which doesn't bode well for flows to emerging markets, but there is more fundamental problem out here which is the emerging market growth model is sort of under serious question and this is what is going back to my earlier point about Trump presidency with two changes that they are going to make or are very serious about making. One of them will pass for sure, the other one, I am not sure but this has major implications for India. Take the first thing that they are going to reduce the corporate tax rate, from 35 or something that they are talking about to 15 or 20 percent, this is huge because here is the largest market in the world which is reducing its corporate tax rate from 35; effective it is a bit lower but 35 is the top rate down to 15-20 or something, so that is huge because why would anyone invest outside their domestic market and it is so large, when the corporate tax rate is being brought down dramatically.

Q: So that is not an issue as far as the foreign institutional investors (FIIs) investment is concerned but even FDI investment for countries like India?

A: As far as India is concerned - that's what even I said two years ago - the first thing that India needs to do is to bring down its corporate tax rate.

Q: While the growth map is 25 percent that the finance minister laid out in his first Budget.

A: Yes but that was very incremental and now if you do not do something dramatic on corporate tax rates.

Q: What would dramatic be for you?

A: If the United States is going to reduce its corporate tax to 15-20 percent and if we do not bring it down to at least a similar level, I think that is going to be a big trouble. Why would you want to setup plant or factories here or at least a US person would want to do it, if the corporate tax rate in the United States is going to be 15-20 percent, so that is a major change which is taking place.

Q: You think that the government ought to bite this bullet even in this Budget?

A: Absolutely and this is where you have the long-term consequences of demonetisation because what is happening today is that the focus is now shifting to what sops to offer to try and make up for whatever hardship that the poor have gone through and the sentiment has been a bit more anti-rich.

Q: In that context to do a significant corporate tax rate you believe will be in question?

A: I think so but for me this is the economic necessity, this is the need of the hour that you need to match those corporate tax rate because the US used to have highest corporate tax rate in the world and now from 35 they are going to go to 15-20 percent - that is like a dramatic shift and if you do not match that that is going to have a serious implications - that's one. So the corporate tax rate cut of 15-20 percent is a very high probability that's going to happen in the US. The second is much more controversial but with even greater implications for India which is that they are discussing something called destination tax. The destination tax implication is that exports are going to be tax-free and imports are going to be taxed - that's a very crude way of putting it but that is what they are talking about. If that were to go through - that would mean the entire outsourcing model to emerging markets or even exporting your way to prosperity model which is how many emerging markets have grown rapidly, Korea, Taiwan, China - that model is going to be seriously impaired.

Q: But this impacts the US economy itself, doesn't it. Do you believe that this is going to be something that perhaps they will tempo?

A: Yes. So this is like something they are facing opposition for but what is very clear is that America from an economic standpoint is turning much more invert. It is about how we get investment back into our country because investment has been so weak out there for a long period of time and you have a very business friendly government that has come into place just now; a whole host of businessmen out there. So this is the business friendly government that America has had in a long time, some people possibly say ever and they are very focused on these kind of things as to how to get investment back in; lower corporate tax rates, possible border tax, repatriation of overseas earnings, profits, so that's the way they are moving. However, eventually you can argue that American cannot live in isolation if the rest of the world doesn't do well, the dollar surges too much - that is going to hurt them but for the next year or two that is the dynamic, that is what is going to happen and this is where we need to wake up which is to get out of our insular mindset and say that this is how the world is changing, how do we respond to this change.

Q: One response you said is that for India to be more aggressive when it comes to bringing down its corporate tax rates, you believe this 25 percent is not going to work, much more radical action needs to happen and it needs to happen perhaps as soon as Budget 2017.

A: Yes.

Q: What else?

A: I think that our entire model of exporting our way to prosperity is something under serious threat because we are in the world of deglobalisation and in this to rely on external capital much to fund our growth that is something that the government spoke about, we just have to be mindful that yes, that is how it used to work but that model today is seriously impaired.

Q: So encourage domestic investments which haven’t picked up?

A: Exactly but to expect much more FDI or foreign investment to flow into India, I am not very hopeful of that because we are in a deglobalising world which means that the trade flows are going to remain weak for a long period of time across the world and also capital flows are going to remain weak across the world. In that environment, you have to focus much more on the domestic economy and exporting way to prosperity that model has been seriously impaired. The developing ladder from just being like this has basically gone vertical. So it is going to be much harder to grow. Even in terms of bringing back black money and doing these kind of things, I think that once again I wish we had sort of learned from our own experience of the past and what other countries are doing like Indonesia -- Indonesia wanted to bring back black money so they decided to have a penalty rate of just 4 percent and they got USD 300 million including the former President Suharto -- one of the biggest crony capitalist leaders, his son brought in USD 30 billion. So it depends what we want to achieve.

We are a capital starved economy, if we need more capital, it is getting more and more difficult in the global market place. How do you attract capital flows in this? It is best if you attract your own money back, which is in terms of overseas money but today in terms of the message is -- if you speak to businessmen, they are still figuring out how to keep a lot of their wealth overseas rather than bringing it back.

Indonesia did the opposite, in fact, they have been criticised a lot, it is the other extreme, 4 percent penalty rate and you can bring back whatever money you want. They did that under the scheme and they got USD 300 billion dollars so that is like an abundance of riches but see how the mechanism works because they got that much capital in, now they are being able to cut interest rates, the currency has stabilised even though they have a much larger current account deficit as a share of gross domestic product (GDP) than India does.

Q: That is the argument the government is presenting even as far as this particular scheme is concerned, there is now an income declarations scheme Part II?

A: At 50 percent of those kind of rates, this has not worked globally. That is a global experience. Maybe in India, it will function but globally at those rates, you don’t get much traction. So, Indonesia does it at 4 percent, you get massive money in but then that has political problems and all that. So I think that this is what we need to do. So for me, that is the important part that these experiments going on across the world, all we have to do is to basically borrow.

As far as Prime Minister Modi was concerned, when he first came into power in May 2014, I remember I wrote in Wall Street Journal back then in the US that this is India's Regan Walker moment and my optimism was that -- he was speaking a lot about minimum government, maximum governance and he had someone like Raghuram Rajan along with him that this combination could be great for India in terms of potentially what it could be. I had some reservations about it but potentially what it could be so I think that is what we were hoping and then even then after that we kept wondering that which global leader will Modi be like, the things like demonetisation are not from the global leaders' playbook. That is my point.

Q: He is writing his own playbook, that is what he said?

A: That is fine but I want to say that as far as I am concerned, I think that my basic difference is the fact that we don’t need to write our own playbook out here, these global experiments are going on, we are at a basic level of economic development. We have to follow the best practices of what other countries are doing and then we can move on. There are some places where you can argue that things are out of whack in India and we need to do something.

So the other thing which I have been speaking about the last couple of years is the scope of privatisation -- I thought that something bigger would happen as far as privatisation is concerned because this is still an economy where the state is very large and very dysfunctional in many parts, the harassment that ordinary people face has a lot to do with the fact that the state is dysfunctional in India in the way that they interact with it.

Take the banks, there is no other country in the world that I know where the share of assets held by the public sector is as large as India that in India the share of assets in the banking system held by the public sectors is close to 70 percent. There is no democratic nation in the world which does that. The average for emerging market is more like 30-33 percent. So why are we bringing that down in terms of what needs to be done?

So I think in terms of what India can do -- for me the path is quite straight forward but politically I don’t know what is going on anymore because I don’t know -- if you change the narrative now because if the average person is reacting well to this -- I have no idea what exactly is going on currently -- if the average person is saying like he is getting this sort of real thrill that the rich person is being suffered, there will be good politics but from an economics standpoint, I don’t think that is going to be great for the nation.

For the nation, what we need currently if we have to become globally competitive and to grow at the rates of 7 percent which is so difficult to do in today's environment on a sustained basis at the time when the global economy is growing at 3 percent, is that we need to basically react to the international environment, we have to cut our corporate tax rates very sharply, we need to privatise our bloated public sector and also if you want to bring money back in, how to incentivise people to come back into the country and that needs to be done with more carrot than sticks like more incentives rather than disincentives.

Q: The case that you presented, what does it mean in terms of capital allocation, where would India stack up then for instance as far as your emerging market fund is concerned as we look ahead?

A: As far as we are concerned, we are pulled back because I don’t know how the next 12-18 months this country is going to pull out.

Q: Not even the top 5?

A: There are other places where the recovery stories are a bit better like Eastern Europe for example where we find a lot of opportunity because Europe is doing better. In southeast Asia, I am quite impressed with the reforms that Indonesia is doing, Philippines despite everything that the President says in public and politics on the economic front, they are doing relatively good job and then in Latin America there is opportunity.

In Mexico the currency has never been this cheap in its history. It is super comparative as far as Mexico is concerned. So you are finding these kind of stuff but in general, this is a difficult environment for emerging markets because US has decided to totally change the game and I think that the implications of that are being felt. So that is the reasons, over the last five-six weeks, why we have had such a strong rally in United States and it has not been matched by what is happening in emerging markets.

Emerging markets have done nothing over this period even as United States has rallied very strongly and I think that the threat of protectionism is very real but there are different ways it is not going to come. It is not going to come in the classic way of more tariffs and stuff but these non-trade tariff barriers is how it is going to come and changes in the tax regime are possibly going to be a very big deal now.

Q: Since we are talking about the US and how the US in a sense is re-drawing the rules of the game let me talk to you about your other favourite subjects which is China and what this does in fact to China because if the Fed continues to hike and the commentary seems to suggest that we should be prepared for at least three hikes come 2017, what does it do to China?

A: China is still the biggest risk to the global economy.

Q: So, you believe the next recession will still be made in China?

A: Like in terms of - the developed world has seen its worst in terms of what had to happen. Europe has already suffered two recessions last 7-8 years. Japan has basically become inconsequential with no growth because it has a serious demographic issue and then you have the United States where the animal spirits have just been revived so late in the economic cycle. They have been growing at 1.5-2 percent. Now all of a sudden you are going to get at least some blip up because of the big revival in animal spirits. So, as far as China is concerned it is a real problem at two levels.

Today there is one statistic about China which you should remember that it takes USD 4 of debt to create USD 1 of GDP growth in China. At the peak of the US housing bubble it took USD 3 of debt to create USD 1 of GDP in the United States. So, this is a mother of all bubbles that we are seeing in China as far as the increase in debt is concerned. And then because they want to keep the debt going the amount of money is circulating in China today is 40 percent larger than the money in the United States. So, you have a huge amount of money circulating in China which is creating all sorts of domestic bubbles in China but it all wants to get out in terms of a lot of it. So, a lot of the money is leaving China and they keep putting up gates out there to try and block this from happening but as United States increases interest rates that wall of money will continue to leave and at some point of time China will really have to face the music here because if you are going to have such a huge creation of debt and then all of a sudden your ability to create that is going to be limited because money is leaving your country that is going to have serious implications for the global economy.

So, as a look out at 2017 the momentum today is with the developed markets. And as far as China is concerned it remains the biggest risk to the global economy and as far as EMs are concerned lucky this is 35 percent of the global economy, they can keep finding some spots to do well but the growth models in a lot of stuff that we believed about EMs for the last 20-30 years are being seriously challenged today by the way the global economy is shifting. With de-globalisation now the big buzz word around the world.

Q: And a very real threat?

A: Yes and it is already happening. Even before these elections took place of Trump deglobalisation was already sort of on its way.

Q: You were talking about whether this will in fact reap dividends for the BJP politically or not and outside of economics you also spend a lot of time on the election yatra, you cover state elections as well. UP is coming up. Do you believe that this narrative is going to work for them politically, a lot of people are comparing this to the days of Indira Gandhi and Garibi Hatao and whether Modi is actually positioning himself in that sort of avatar. Do you believe that this is going to pay dividends politically for them?

A: I have no idea as yet. Because I think we haven't heard much from what is happening on the ground in UP apart from some people who have been there and they all think that there is economic distress but at the same time they also come back with reports.

Q: The BJP holds up the municipal election results as sort of a vote of approval for demonetisation so on and so forth.

A: Yes, but in the past though having looked at Indian elections those election results have been very poor forecasters of what happens in the main election by the way. So, I wouldn\'t read too much into it. But having said that the anecdotal evidence is that a lot of people are quite tolerant of this thing that they are saying that yes because they think that this is a bold step they think that this is something which is right because it is sort of very emotive thing that you are basically soaking this corrupt rich people. So, that is good like in a way. That is what happened in 1970s also back here in India.

However, in terms of what is going to work today I don't know but here is what we know about UP that my own feeling is that it is very much going to be an election dominated by the traditional factors of cast but we in the media and everybody is going to portray that election as a referendum on demonetisation.

Q: Which is missing the woods for the trees.

A: Yes, but I am not sure that is going to be a big factor in the election because cast is so important and in terms of what is going to happen out there. So, this is going to be a fascinating thing that even though the election where we won and lost in UP based on the cast arithmetic in terms of it where everyone is debating where would the Muslim vote go this time, if it goes to Mayawati she is home, if it doesn't go to her then the BJP has a chance if they are able to split the vote between the Congress-SP kind of combined.

So, elections would be fascinating, I am going to come back to India at the end of February to basically travel to UP. In fact I think it will be our 25th election trip that we have done over the last 20 years and seven of them I have done to UP because there is no state like UP for politics. You can sort of stop at any Dhaba in UP and get people very activated about politics. But it is very much still about cast arithmetic in that state. So, I am not sure demonetisation will be such a big issue on the ground there. But we in the media are going to portray that as a referendum on demonetisation. But what is happening regarding cast arithmetic I don't know as yet. I want to go with an open mind. When we do go in February to travel across UP.

Q: What would be the key inflections points, what would be the key risks that you would watch out for in 2017?

A: As I said what is happening like the United States has major global implications particularly for India. How are we going to respond to that.

12.09.2016

DOW @ Record Highs: Why Shouldn’t One Fall In Value Trap?

With the US

equities firmly setting themselves up around all time highs, the doomsday predictions

have started flowing in. This is typical scare mongering which has been

witnessed every time a prominent trend stays in place for a sustainable period

of time. Equities have been remarkably resilient this year, factoring in fallout from events like Brexit and the Trump victory. However, “While the S&P 500 is reaching all-time highs on

optimism over Donald

Trump's economic agenda, some Wall Street strategists are increasingly

worried about a widely followed valuation measure that's reached levels that

preceded most of the major market crashes of the last 100 years” , (http://www.cnbc.com/2016/12/08/market-indicator-hits-levels-last-seen-before-plunges.html

)

To be sure, the valuations have been elevated. But is that

a good enough reason for the bulls to start offloading their prized

possessions? The article says that the Shiller "cyclically adjusted

price-to-earnings ratio" (CAPE) is calculated using

price divided by the index's average historical 10-year earnings, adjusted for

inflation. Yale economics professor Robert Shiller's research found future

10-year stock market returns were negatively correlated to high CAPE

ratio readings on a relative basis. He won the Nobel Prize in economics in 2013

for his work on stock market inefficiency and valuations.

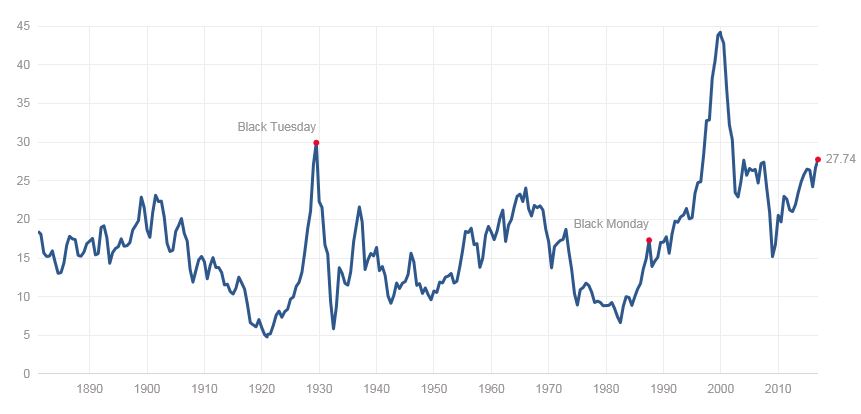

Here is the chart being refereed to…

Shiller CAPE PE Ratio

While the article is right in pointing out that the current

levels have been exceeded only thrice in last one century, the difference in absolute

values on the chart over last one decade is puzzling. The CAPE

strode up to near 45 levels at the height of the 2008 debt fueled rally. The

metric currently stands at just about 28 now. One more important point to

consider is the alarming spurt in global central bank assets. Major central

banks have witnessed a tremendous spike in their balance sheets in the aftermath

of the global financial crisis. The aggregate size of major central assets is

up from $5.5 Trillion to $18 Trillion over last eight years.

Coming back to the CAPE, it is important to note

that the value of the metric has been elevated over last two to three years. In

fact, in September 2014, when US stocks were rising in a similar manner and looking

unusually expensive, Rober Shiller himself stated that 'We saw this before the

Wall St crash, the dot-com bubble and the credit crunch". Will the CAPE hold true this time or investors would fall in a value trap? ...only time will tell! Read

more: http://www.thisismoney.co.uk/money/investing/article-2742297/PROF-ROBERT-SHILLER-INTERVIEW-How-stocks-crash-2014.html#ixzz4SLTBjsva.

.

Subscribe to:

Posts (Atom)